Calculating Benefits

Now is the time to prepare for the future!

The hours you work count in several important ways. They help determine when you become entitled to receive a pension from the Plan, and they also help determine the type and the amount of your pension.

You earn pension credit when you are working in a job covered by a collective bargaining agreement or other participation agreement that requires your employer to make contributions to the Fund on your behalf. (See Future Service Credit below.)

You do not generally earn pension credit when you work for an employer who does not have an obligation to contribute to the Fund. However, you may earn pension credit for such work if the employer later becomes obligated to contribute to the Fund. (See Past Service Credit below.)

Also, when you work in the jurisdiction of a Local Union that is signatory to the United Association Pension Fund Reciprocal Agreement, employer contributions received by the away-from-home fund may be transferred to the National Pension Plan on your behalf. In that case, you will receive pension credit.

Future Service Credit

Future service credit is the pension credit you earn after your contribution date – in other words, it is credit you earn for covered employment after your employer begins contributing to the plan.

Your contribution date is the date that your first contributing employer, in the jurisdiction of your home Local Union, was first obligated to make contributions to the National Pension Plan.

The amount of future service credit you earn is based upon the number of hours you work in covered employment each calendar year as shown in the table below.

For calendar years before 1999, you could earn a maximum of 1 year of Future Service Credit. For 1999, you could earn a maximum of 1.1 years.

Beginning in the year 2000 you can earn a maximum of 1.2 years of Future Service Credit.

Starting in calendar year 2024, there is no longer a maximum of 1.2 years of future service credit that you can accrue per year. Also, the threshold number of hours of work needed to accrue 1.2 years is reduced from 2100 to 2080. You accrue an additional .1 year for each additional 300 hours of work above 2080.

|

Hours of Work in Covered Employment During Calendar Year * In or After 2024 |

Year of Future Service Credit |

|---|---|

|

For each additional 300 hours in excess of 2,380 |

Additional 0.1 |

|

2,380 to 2,679 |

1.3 |

|

2,080 to 2,379 |

1.2 |

|

1,800 to 2,079 |

1.1 |

|

1,500 to 1,799 |

1.0 |

|

1,350 to 1,499 |

0.9 |

|

1,200 to 1,349 |

0.8 |

|

1,050 to 1,199 |

0.7 |

|

900 to 1,049 |

0.6 |

|

750 to 899 |

0.5 |

|

600 to 749 |

0.4 |

|

450 to 599 |

0.3 |

|

300 to 449 |

0.2 |

|

150 to 299 |

0.1 |

|

Less than 150 |

0.0 |

Past Service Credit

Past service credit is pension credit earned before your contribution date. It is credit for work performed by you in a job classification before contributions were required to be made to the Plan for that same work in that Local Union.

You may be eligible for past service credit if you were actively employed in a bargaining unit’s jurisdiction when the unit began to participate in the National Pension Plan, and if you had been employed on a fairly regular basis in the bargaining unit’s jurisdiction before contributions begin.

Past service credit is also available to employees of employers that are new signers of a collective bargaining agreement that requires contributions to the National Pension Plan. If this applies to you, you may receive past service credit for work you did for this employer before the effective date of the collective bargaining agreement, if such work is now covered by the National Pension Plan. Participants with contribution dates on or after January 1, 2000, only qualify for Past Service Credit if they attain five years of Future Service credit or five years of Vesting Service after their contribution date.

In general, you earn one year of past service credit for any calendar year during which you worked at least 750 hours with an employer or employers that later agreed to contribute to the National Pension Plan. If you worked between 375 and 749 hours, you earn one half year of past service credit.

The maximum years of past service credit you can earn depends upon your contribution date. See the Summary Plan Description for details. Participants with contribution dates on or after January 1, 2000, may earn a maximum of five years of Past Service Credit.

The Past Service Credit Employment work history forms or Local pension fund records generally are the best sources of Past Service Credit information.

Benefit Calculations

Benefit Schedules

Separation

A vested participant who incurs five or more consecutive years without any Future Service Credit incurs a Separation. Prior to 2004, accrued benefit for credit earned prior to the Separation is at the highest contribution rate negotiated by the participant’s home Local Union for this work (for which he or she has at least 1,500 hours of work) at the time of his or her Separation. The benefit schedule used is the schedule in effect at the time of the Separation. Separations can also occur for non-vested participants in certain cases and are different than permanent breaks-in-service.

Permanent Break in Service

Age at Retirement

The Fund’s normal retirement age is 65. If you are eligible to retire at or after age 62, however, you will receive full benefits, which are not reduced because of your age.

If you retire before age 62 but at or after age 60, you will see a 1½ percent per year or 1/8 of 1 percent reduction per month. If you retire before age 60 but at or after age 55, you will see a 6 percent per year or ½ of 1 percent reduction per month.

Age 55 is the earliest retirement age unless you are totally and permanently disabled and qualify for a disability pension.

Benefit Types and Options

The UANPF provides multiple types of benefits and options for participants:

- Normal form of benefit for single participants: Single Life Pension with 5-Years Certain Payments

- Normal form of benefit for Married Participants: 50 percent Joint and Surviving Spouse Pension.

- Many other benefit types and options: See Summary Plan Description for more details

Benefit Calculation Example

The following examples will illustrate how a participant’s benefits from the United Association National Pension Fund (UANPF) are calculated when they include work before 2005, as well as work in the years following 2005. The document Plan Changes Beginning January 2005 provides additional information.

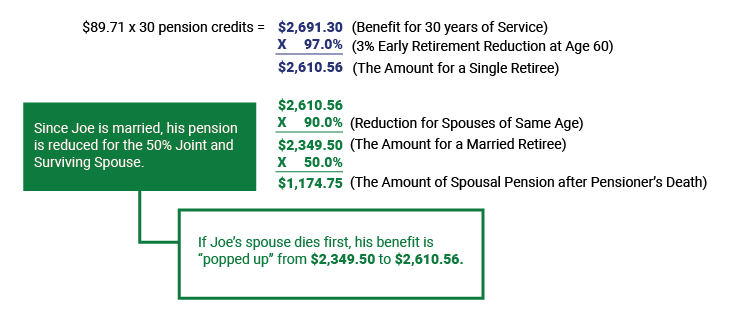

Example 1

Joe is 60 years old on January 1, 2005. His Local Union started participating in the National Pension Fund in 1984. In 2004, his Local Union had a contribution rate of $3.15 per hour and Joe had at least 1,500 hours at this rate in December of 2004. Joe had 10 Past Service Credits and 20 Future Service Credits. He always worked in his home Local Union jurisdiction. Joe is married, and he and his wife are the same age. If Joe had retired effective January 1, 2005, his benefit would have been calculated as follows:

Since all of Joe’s 30 years of Pension Credit was earned prior to 2005, his benefit is calculated using Schedule A. The contribution rate of $3.15 per hour provides a monthly Normal Pension at age 65 of $89.71 per year of Pension Credit.

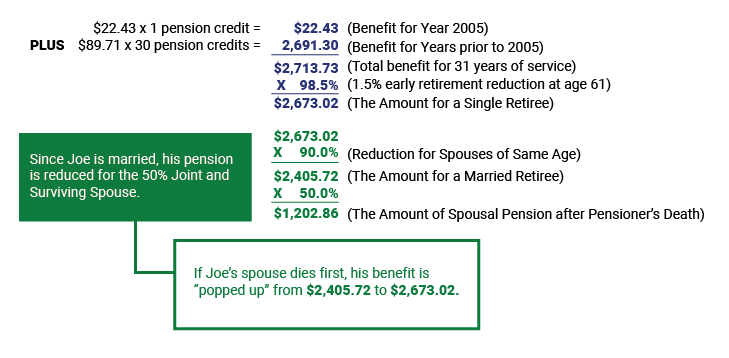

Example 2

Same as above but Joe continued to work during 2005 and earned an additional year of Future Service Credit at the $3.15 contribution rate and then elected to retire effective January 1, 2006 at age 61. With Joe’s one year of Pension Credit earned during 2005, his benefit for 2005 is calculated using Schedule B. The contribution rate of $3.15 per hour provides a monthly Normal Pension at age 65 of $22.43 for this year of Pension Credit, which is added to his previously earned benefit.

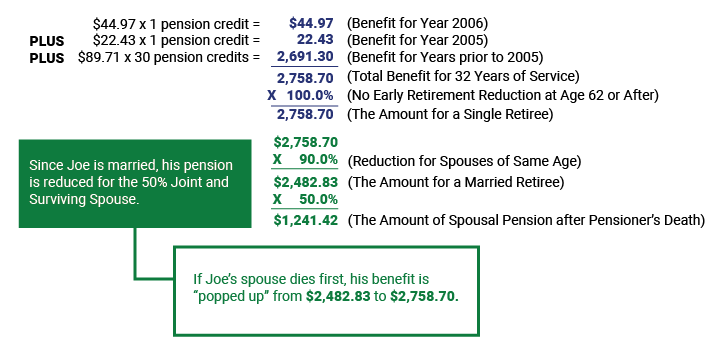

Example 3

Same as Example 2 but Joe continues to work during 2006 and earns an additional year of Future Service Credit. Furthermore, his Local Union increased their contribution rate by at least 25 percent effective January 1, 2006 to a contribution rate of $3.95, and Joe retires effective January 1, 2007 at age 62. With Joe’s one year of Pension Credit earned during 2006 his benefit for 2006 is calculated using Schedule C. The contribution rate of $3.95 per hour provides a monthly Normal Pension at age 65 of $44.97 for this year of Pension Credit, which is added to his previously earned benefit.

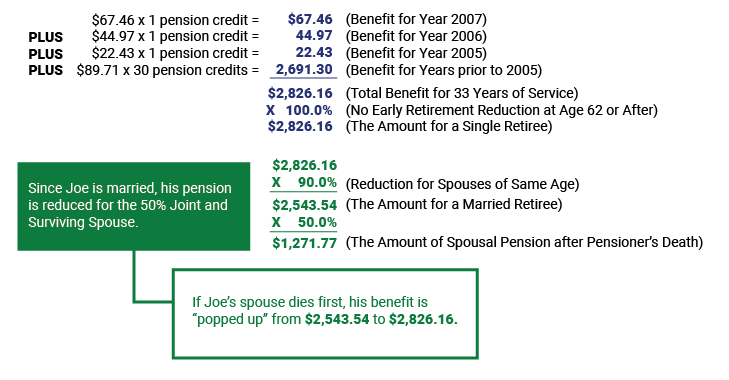

Example 4

Same as Example 3 but Joe continued to work during 2007 such that he earned an additional year of Future Service Credit at the $3.95 contribution rate. Joe then retired effective January 1, 2008 at age 63. With Joe’s one year of Pension Credit earned during 2007 (for work under a collective bargaining agreement with a contribution rate that was at least 25% greater than the rate in effect on December 31, 2004) his benefit for 2007 is calculated using Schedule D. The contribution rate of $3.95 per hour provides a monthly Normal Pension at age 65 of $67.46 for this year of Pension Credit, which is added to his previously earned benefit.

The above examples are offered for illustration purposes and do not apply to every participant. Weighted Average contribution rates, non-standard benefit levels, the timing of rate increases, rate reductions and separations will all affect the benefit calculations. Please refer to the Summary Plan Description for a more complete explanation of the effects of these and other benefit calculation matters.

Note: This discussion of benefit definitions and calculations is simplified for ease of understanding. None of the explanations here takes precedence over the Fund’s Summary Plan Description (“SPD”) or the Full Text of the Plan Rules (“Plan”), and in the event of any conflict between an explanation here and a provision in the Plan, the terms of the Plan govern.